Menu

Stimulating a Settlement, or Two

August 14th, 2025

Sometimes personal injury cases take on a life of their own. The liability is not disputed, or the injuries are obvious and serious, or the insurance coverage is ample, but not so huge that insurers can drag their feet.

My client J’s case was such a case.

At first glance, it appeared not to be an exciting kind of case. My client was older, 81. And while she was hit hard by the other vehicle, her injuries were not obvious or serious at first analysis. And I had no idea what type of insurance liability limits existed.

Then things began to fall into place.

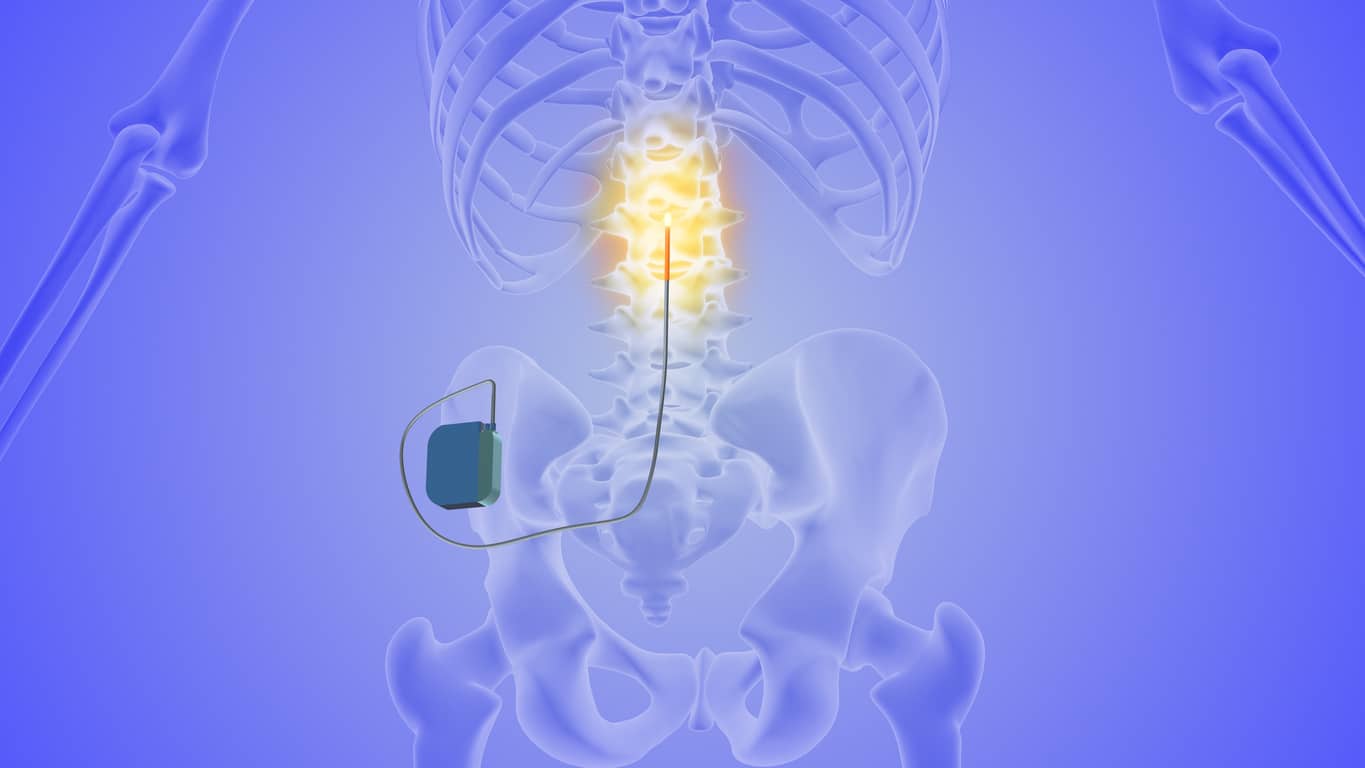

First of all, let’s back up for a moment. J had a previously-implanted spinal device to manage previous back issues. So I’m thinking, oh no, she’s old, pre-injured, and how are we going to be able to tell the difference between new and existing injury?

Then she called me and advised me that her doctor had determined the spinal stimulator had been broken due to the force of the crash. The remedy for a broken spine stimulator is a new one.

How do you get an old spine stimulator out of a person and install a new one? Surgery. Suddenly, the case got a lot more interesting.

Damages And Coverage

Personal injury attorneys like me work on a contingency fee basis. That means I only get paid if I win at trial or achieve a settlement. So the first thing I investigate is who the at-fault driver’s insurance company is, and what level of liability insurance they have.

If you have read my blogs at all over the last few decades, you know there are some cases that involve catastrophic injuries and very little available insurance coverage.

In J’s case, it turned out the other driver had a policy of $100,000. Sounds like a lot of money, right?

What about if you’re an 81 year old who undergoes surgery to get a new spinal stimulator implanted. What do you think that costs? How much does it hurt and for how long? Does it work perfectly right away? And what if this 81 year old has a job to keep her from being bored after retiring?

Well, let’s just say her medical bills alone far exceeded that liability limit.

The “easy part” was getting the at-fault driver’s carrier to tender its full policy limits.

When I was retained, the first thing I did was ask my client what HER auto insurance limits were. So I knew right away her Uninsured Motorist/Underinsured Motorist (UM/UIM) limits were $250,000.

What this meant was that I was tendered the policy limits of the at-fault party and demanded the available limits of the UIM insurer (hers). As I’ve explained before, the UIM policy limits of $250,000 are reduced by the at-fault policy limits of $100,000, meaning there would be UP TO $150,000 additional available.

I demanded this amount from her UIM carrier, making my case with medical records, her ongoing pain, adjustments her doctor had to keep making to her stimulator to reduce her pain. After some adjustments, she is just about where she was before, healthwise, and is back at work.

Settlement Number Two

I did not expect the UIM carrier to tender the entire policy right away.

I expected I’d have to work for it, bargain with them, justify her pain and suffering, loss of a normal life, explain why the full value of her medical bills would come into play in a court of law, rather than what Medicare paid.

It never got to that. I received an email a few weeks after my demand tendering the full $150,000.

The insurance company did the right thing. It valued the case correctly. It didn’t fight, whine, or make any arguments.

It was a legitimate claim, with serious injuries, and not nearly enough insurance to go around.

Was her case potentially worth more than $250,000? Maybe. Is $250,000 a terribly unfair result? Not at all.

In other words, sometimes, the coverage, injuries, and everything else line up just about perfectly for everyone involved.

No one wants to be injured. No one wants to have a spinal stimulator damaged or to have to undergo surgery to replace that. Certainly not at 81 years old! But if it happens, it’s nice when that person receives fair compensation within a reasonable time. Even so, it usually takes a personal injury attorney who understands insurance coverage issues to make it happen.

Takeaways

- Many factors determine how quickly and fairly a case is resolved

- Your own insurance coverage is as important as that of the person at fault in your accident

- Make sure you check your insurance coverage limits after reading this!

Contact Chicago Personal Injury Lawyer Stephen Hoffman

If you have been injured, whether by an auto accident, bike or pedestrian crash, dog bite, work accident, or medical malpractice, seek medical attention immediately. Report accidents to the police and your own insurance company, or to your employer if you were injured at work. Then contact a lawyer with experience in your type of injury matter.

If you have been in an accident and have questions, contact Chicago personal injury attorney Stephen L. Hoffman for a free consultation at (773) 944-9737. Stephen has over 30 years of legal experience and gets results; he has collected millions of dollars for his satisfied clients. He is listed as a SuperLawyer, has a 10.0 rating on Avvo, and is BBB A+ accredited. Stephen is also an Executive Level Member of the Lincoln Square Ravenswood Chamber of Commerce.

Stephen handles injury cases on a contingency fee basis, which means you pay nothing up front, and Stephen only gets paid if you do. You have only a limited time to file a claim, so don’t wait another day; contact Stephen now to get started putting your life back together.